Fleets spend serious money on driver safety, training, telematics, and preventive maintenance. And it works.

But insurance premiums keep climbing anyway.

That’s not because fleets aren’t doing enough. It’s because one of the biggest loss drivers still sits outside the normal safety stack: weather. It changes fast. It hits mid-route. And it often shows up in claims as “driver error,” even when the real trigger was wind, ice, flooding, or extreme heat.

Here’s the business case in plain terms: weather intelligence turns environmental exposure from a surprise into a managed variable. When you reduce exposure, you cut crash frequency. When you cut frequency and severity, you improve loss ratios. And when your loss ratio improves, underwriters treat you differently at renewal. That’s where the insurance savings come from.

If you want to operationalise it, weather intelligence is available through the Geotab Marketplace using “Order Now,” and weather alerts can run through the CrewChief mobile experience, including Weather by CrewChief and the CrewChief Mobile App listing. For fleets that want a direct path to enablement and support, start here.

Why Weather Is One of the Largest Contributors to Fleet Losses

The hidden cost of environmental exposure

Weather doesn’t just cause wrecks. It creates expensive chain reactions:

- Higher crash frequency during storms, ice events, and heavy rain

- Higher-severity collisions when visibility drops or roads glaze over

- Cargo spoilage from temperature swings and delays

- Mechanical strain from heat, cold starts, and stop-and-go congestion

- Downtime from closures, detours, and recovery events

And the problem is scale. Federal transportation research has shown a meaningful share of crashes occur during adverse weather or on slick pavement. That matters because underwriting is math. If a fleet operates in high-exposure corridors and seasons, insurers price that risk in—whether the fleet tracks it or not.

How insurers price weather risk

Insurers don’t pull a weather line-item out of a hat. They look at:

- Historical loss experience (your claims history and severity)

- Exposure profile (where you operate, how often, and when)

- Vehicle mix (high-profile units, hazmat, temperature-controlled)

- Safety controls (what you can prove and document)

If weather risk stays undocumented, it doesn’t disappear. It just shows up indirectly as volatility: spikes in claims, unpredictable severity, and reserve pressure. Underwriters hate volatility.

The financial impact of doing nothing

When a fleet can’t show controls for environmental exposure, the default assumption is simple: “You’re exposed, and you’re reactive.”

That usually turns into:

- Premium creep year over year

- Less flexibility on deductibles and coverage terms

- More scrutiny on safety narratives at renewal

- Fewer options when the market tightens

What Is Proactive Weather Intelligence?

From reactive to predictive risk management

Most fleets handle weather like this:

A driver calls in. Dispatch reacts. Operations scramble. Everyone hopes the timing works out.

Weather intelligence flips that. It adds “what’s coming next” and “where exactly” to the decision making process.

Instead of responding after conditions hit, you can plan around forecast windows and route-level risk.

Core capabilities of weather intelligence platforms

A strong platform typically supports:

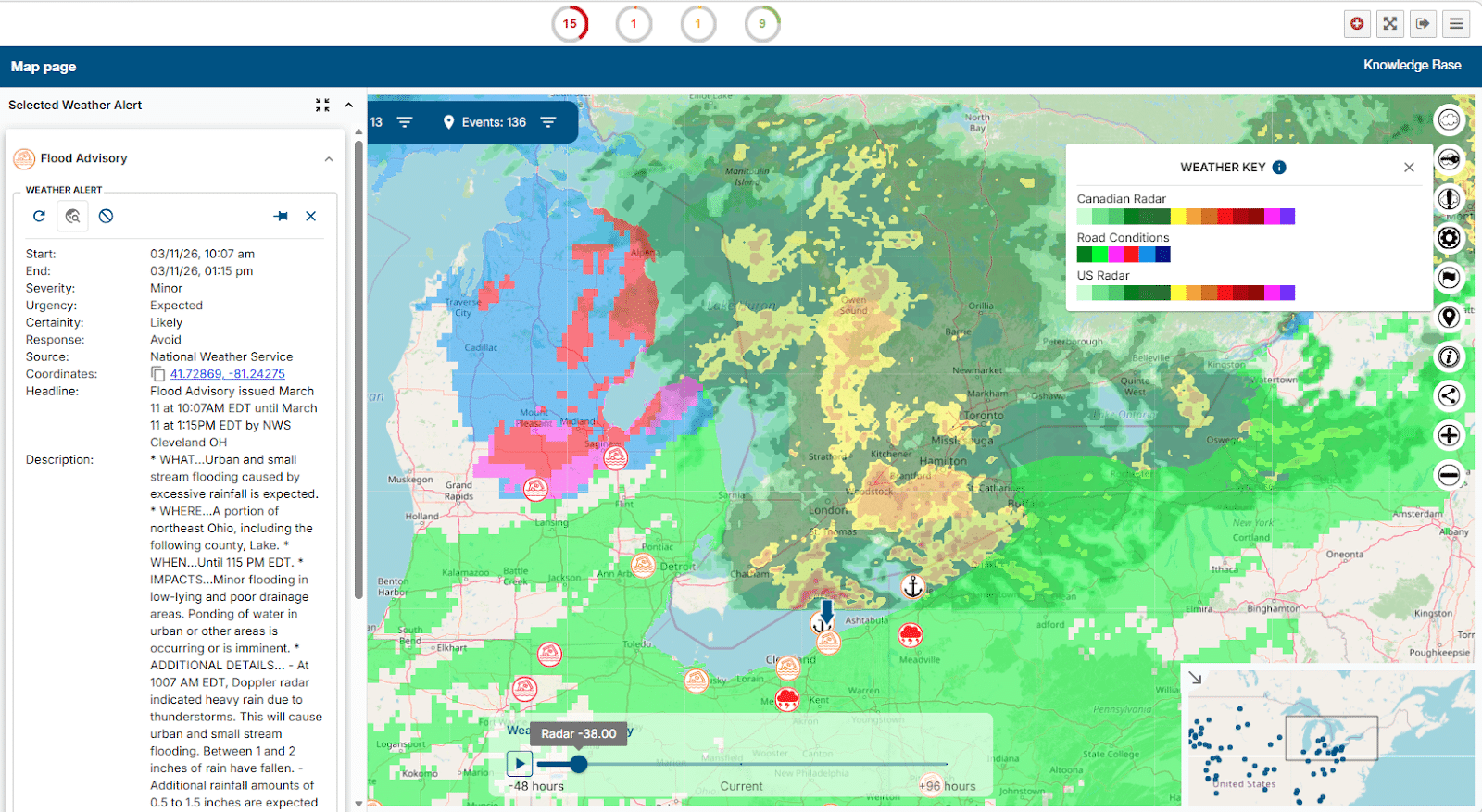

- Real-time hazard alerts (wind, ice, flooding, lightning, extreme heat)

- Forecast-based planning windows (so dispatch can build safer plans)

- Route-level risk analysis (not just city-wide “rain” icons)

- Dynamic routing guidance and avoidance thresholds

- Operational playbooks (delay, reroute, stage, swap equipment, adjust schedules)

This is where weather becomes controllable. Not controllable like a machine. Controllable like a risk lever.

Turning weather into a controllable variable

Insurance carriers reward what you can prove. Weather intelligence creates proof:

- Timestamped alerts sent to the driver or dispatch

- Documented reroutes and delay decisions

- Records showing exposure was reduced before an incident occurred

That documentation matters almost as much as the avoided incident, because underwriting runs on evidence.

How Weather Intelligence Directly Reduces Insurance Costs

Fewer claims, lower severity

Insurance savings don’t require perfection. They require trend lines.

When weather intelligence reduces exposure, you typically see:

- Fewer weather-related collisions

- Fewer “catastrophic” events (rollovers, multi-vehicle pileups, jackknifes)

- Better protection for high-value cargo and equipment

- Faster response and recovery when an incident does occur

Even small reductions in severe events can move your loss picture dramatically.

Improved loss ratios (in plain English)

A loss ratio is basically:

Claims paid + claim reserves ÷ Premium

If claims rise faster than your premium, your loss ratio worsens. Renewals get ugly.

If you cut claim frequency and severity, your loss ratio improves. That gives your broker leverage at renewal.

Stronger underwriting position

Underwriters want to know:

- Are you exposed?

- Are you managing the exposure?

- Can you prove it?

Weather intelligence supports all three with usable, auditable data. That can reduce “unknown risk,” which often carries a pricing penalty.

Why Insurers Reward Proactive Environmental Risk Management

The shift toward risk-based incentives

Commercial auto insurance has moved deeper into data-driven underwriting. In many market outlooks, carriers emphasize tighter underwriting, more scrutiny, and a continued focus on measurable risk controls.

Telematics became common because it measured behavior. Weather intelligence fits the same logic because it measures exposure and mitigation.

Insurance benefits fleets may unlock

Not guaranteed. But realistic, depending on loss history and carrier appetite:

- Improved renewal terms

- Better negotiation on deductibles and SIR structures

- Stronger eligibility for safety incentive programs

- More competitive quoting interest in tough markets

Competitive advantage in a hard market

When underwriting tightens, fleets with proof win. Fleets with assumptions lose.

If two fleets look similar operationally, the one with documented environmental mitigation often looks “more controlled.” That’s the entire game.

Weather Intelligence Completes the Modern Fleet Safety Stack

The three pillars of fleet risk management

Most fleets already manage:

- Behavioral risk (telematics, coaching, Dashcam Solutions)

- Mechanical risk (Fleet Maintenance, inspections, preventive programs)

Weather intelligence is the third pillar:

- Environmental risk (hazard avoidance, exposure tracking, proactive decision support)

If you only manage two pillars, you still carry uncontrolled loss drivers.

How integration multiplies results

Weather intelligence gets stronger when it ties into the rest of the stack:

- Telematics tells you how a driver behaves.

- Weather tells you what the environment demanded in that moment.

- Maintenance tells you whether equipment was stressed and needs attention.

That combined view improves investigations, coaching, and renewal narratives.

Operational Benefits That Strengthen the Insurance Argument

Beyond claims, weather intelligence tightens day-to-day operations in ways underwriters respect. Dispatch avoids closures and high-risk corridors before trucks get trapped, which cuts detention, missed appointments, and weather-driven overtime. Route adjustments reduce idle time and fuel waste when congestion builds around storms.

Temperature-sensitive loads stay protected because teams plan around heat, cold, and delay windows instead of reacting after spoilage risk rises. Equipment also lasts longer when drivers avoid severe conditions that accelerate tire, brake, and cooling-system stress. The result is steadier performance, fewer disruptions, and cleaner documentation you can tie back to measurable outcomes.

Reduced downtime and disruption

Fewer road closures. Fewer surprise detours. Less “stuck out there” time.

That steadiness reduces secondary losses like missed appointments, service failures, and rushed driving.

Lower fuel and operational costs

Weather-driven detours and idling burn money.

When dispatch avoids the worst windows and routes, you often reduce:

- idle time

- stop-and-go congestion exposure

- deadhead and reroute waste

Cargo and asset protection

Weather intelligence supports better decisions for:

- temperature-sensitive freight

- high-value loads

equipment that cannot sit in flood zones or extreme heat

Driver retention and safety culture

Drivers don’t love white-knuckle miles.

When operations supports smarter calls—pull over, delay, reroute—drivers feel protected. That shows up as better compliance, fewer risky “push through it” decisions, and stronger retention.

ROI Framework: Quantifying the Financial Impact

Cost avoidance calculation

Start with your baseline:

- Total claims per year

- Weather-adjacent claims (ice, wind, flood, heat, visibility)

- Average severity (and worst-case events)

- Downtime cost per incident (including recovery and missed service)

Then track:

- avoided high-risk miles (exposure reduction)

- alerts issued and actions taken

- incidents prevented or reduced in severity

Insurance savings projection

Keep it conservative:

- Best case: meaningful reduction in severe events

- Expected case: steady improvements over 2–3 renewals

- Worst case: improved documentation and underwriting narrative even if the year is volatile

The compounding comes from better loss ratios across multiple cycles.

Sample business case structure for fleet leaders

Build a one-page internal memo:

- Baseline: loss runs + top weather-related loss categories

- Exposure map: routes, seasons, and high-risk corridors

- Controls: what you do today (and what you can’t see)

- Weather intelligence plan: alerts, thresholds, workflows

- KPI targets: exposure reduction, response time, severity reduction

- Renewal strategy: how you’ll present documentation to underwriters

If you want this to land, tie it to renewal timing. Start tracking before the broker asks for it.

Strategic Implications: From Safety Tool to Insurance Strategy

Weather intelligence is a risk-management lever

This isn’t just “nice routing.” It’s a measurable control that influences insurability.

It gives you a way to show: “We don’t just react. We mitigate.”

Positioning for future volatility

Weather patterns have grown more disruptive in many regions. Underwriters respond with higher scrutiny and tighter terms. Fleets that can document mitigation stay more stable through the swings.

Why “nice-to-have” tech is now mission-critical

If you operate high miles across variable corridors, weather intelligence isn’t extra. It’s part of the control environment—like preventive maintenance or driver coaching.

Frequently Asked Questions

What is weather intelligence in fleet management?

Weather intelligence is a set of tools that delivers route-level hazard alerts, forecast planning windows, and decision support so fleets can reduce exposure to dangerous conditions.

How does weather intelligence reduce fleet insurance costs?

It reduces claim frequency and severity by helping fleets avoid high-risk zones and document proactive mitigation actions that strengthen underwriting and renewal negotiations.

Do insurance companies recognize weather intelligence as a risk-reduction tool?

How is weather risk different from driver or mechanical risk?

Conclusion: Environmental Risk Control Is Now a Financial Imperative

Weather drives severe fleet losses, but most fleets don’t measure it cleanly. That’s why it stays a blind spot in underwriting conversations.

Weather intelligence closes the gap. It reduces exposure, supports better decisions, and creates documentation insurers can trust.

Bottom line: environmental risk control isn’t just safety anymore. It’s a financial strategy—one that can stabilize premiums, improve renewal terms, and strengthen your long-term risk profile.

If you want to connect this to your current safety stack, start by mapping how Fleetistics fits alongside Dashcam Solutions and Fleet Maintenance so you can show underwriters a complete, evidence-backed approach.